10-for-10: Apple Inc. (AAPL) Enters a 232-Day Window With a Decade of Straight Gains

Apple Inc. is heading into a long seasonal stretch that has delivered gains every year for a decade, just as the stock trades near record territory and investors focus on iPhone-driven growth and AI momentum.

Key takeaways

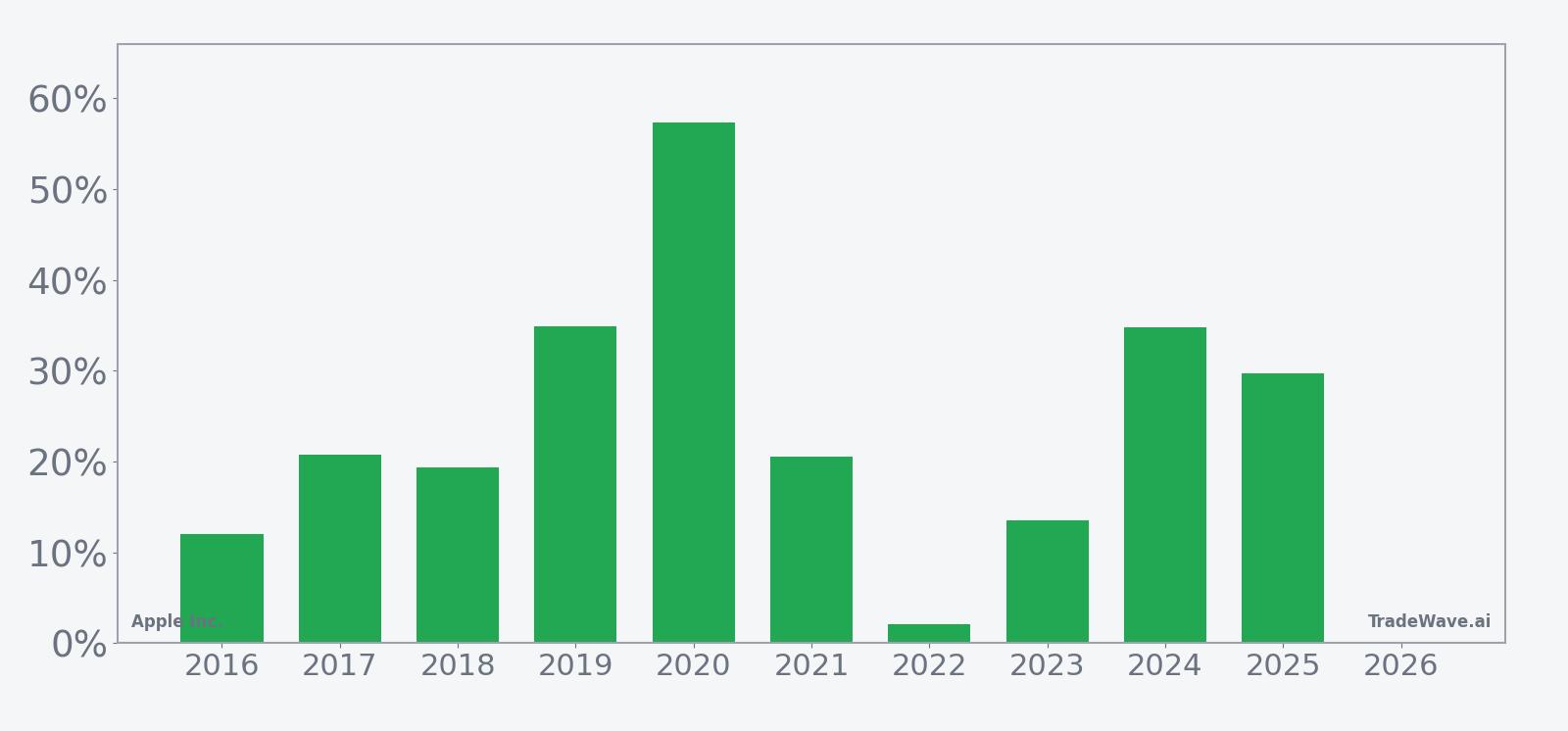

- Apple Inc. has posted gains in 10 of 10 years during this 232-day window, with 100% of outcomes profitable for a long stance.

- The upcoming window starts on Mar 13, 2026 and runs for roughly 11 months, with average gains of 24.51% across the decade.

- Winners have ranged from modest 2.1% advances to a 57.36% surge in 2020, adding up to a 737% cumulative return over the sample.

- The Trade Direction is long, with a TradeWave Ratio of 1.4 and a Sharpe ratio of 1.42, pointing to historically strong risk-adjusted upside.

- Intraperiod swings have been real: the worst drawdown in a winning year reached a 23.51% adverse move before recovering.

- Today AAPL trades at $260.81, about 9.5% below its 52-week high and roughly 55.5% above its 52-week low, leaving room on both sides as the window opens.

According to historical data from TradeWave.ai, this stretch of the calendar has behaved very differently from an average year for Apple, and the next iteration begins on Friday.

Seasonal window

Apple Inc. has risen in 10 of 10 years during this 232-day window, averaging 24.51% gains for a long position. The next window begins on Mar 13, 2026, with the stock last changing hands at $260.81, about 9.5% below its 52-week high of $288.08 and roughly 55.5% above its 52-week low of $167.74. That combination of a strong historical tailwind and elevated but not extreme price levels gives this year’s setup unusual weight for a stock that anchors the major indices.

Across the last decade, the average outcome for this long window has been a 24.51% gain, with a median result of 20.63%. The weakest year in the sample was 2022, when Apple still finished the window up 2.1% after enduring a 14.2% intraperiod drawdown, while the strongest was 2020, when the stock rallied 57.36% and at one point was up as much as 99.45% from the entry level. Add it up and the cumulative return across the ten windows is 737%, a rare clean sweep for a mega-cap name.

The per-year profile shows that this has not been a slow grind higher. In 2016, Apple gained 12.03% in the window but first saw a 12.2% adverse move from the entry. In 2019, the stock advanced 34.9% with a maximum favorable move of 38.5% and a relatively contained 5.94% drawdown. Even the more modest 13.48% gain in 2023 came with a 31.92% peak run-up and almost no downside from the starting point, with the worst intraperiod move just 0.37% below entry.

The 10-year seasonal trend chart suggests that gains have tended to build in stages rather than in a straight line. The typical pattern shows an early push higher, a mid-window consolidation with noticeable givebacks, and then a second leg of strength into the final third of the period. That rhythm lines up with Apple’s product and holiday cycle, where fall launches and year-end demand often reinforce earlier momentum.

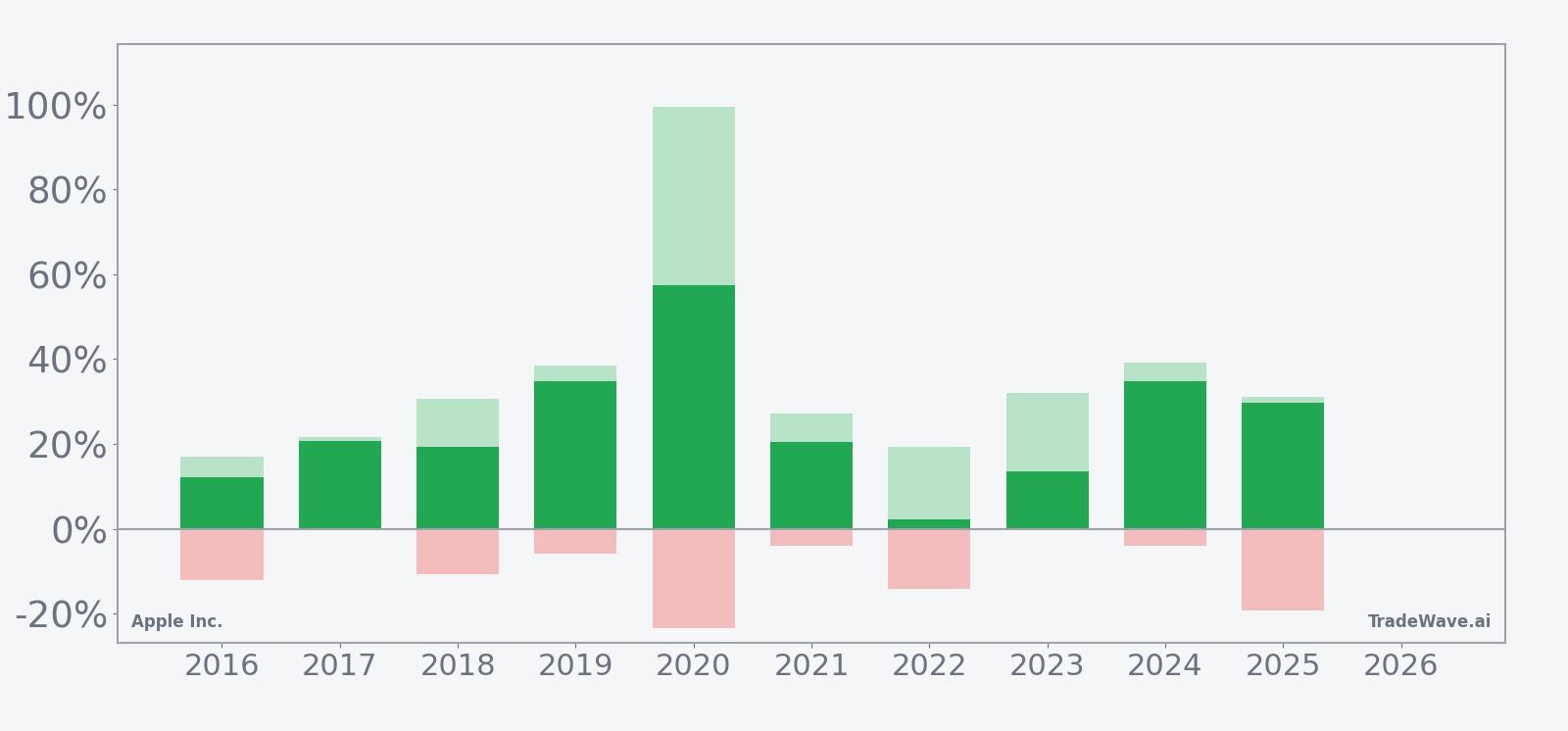

A stacked view of net returns alongside peak run-ups and worst drawdowns shows how much room Apple has historically had to move inside this window.

The combined net, MFE and MAE bars underline how powerful the upside has been relative to the setbacks. In 2020, for example, the stock’s best intraperiod move was a 99.45% run-up from the entry, while the worst drawdown was a 23.51% slide that still resolved into a winning year. Several other years, including 2018 and 2024, show maximum favorable moves north of 30% with single-digit or low-teens adverse excursions. The pattern is clear: this window has favored longs in every year of the sample, but it has not been a smooth ride.

History does not guarantee future results, and even in a perfect 10-for-10 window, adverse excursions can be large before the trend resolves.

Price and near-term drivers

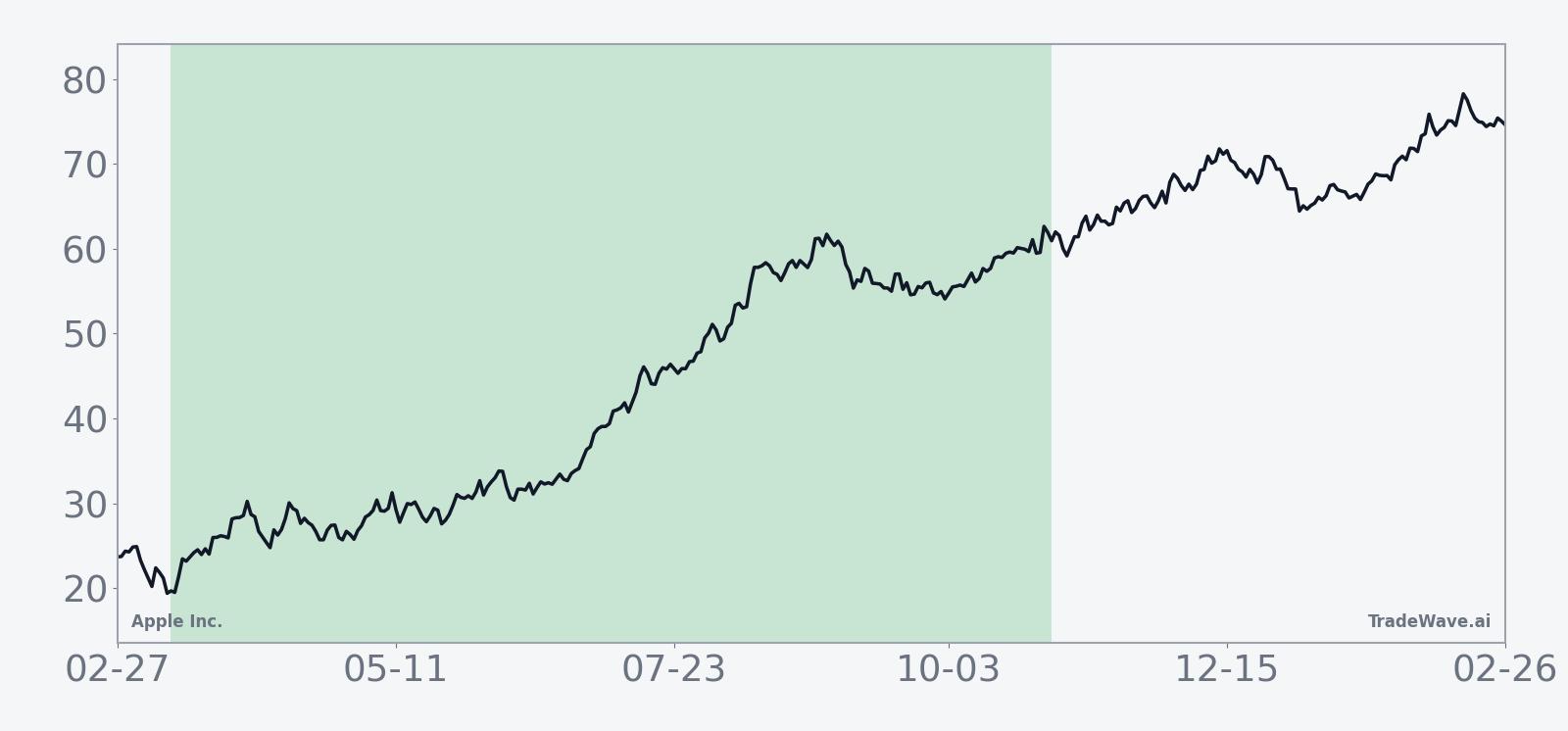

Apple shares closed Thursday at $260.81, down a fraction on the day and sitting about 9.5% below their 52-week high of $288.08 while holding roughly 55.5% above the 52-week low of $167.74. The stock has climbed about 2.48% over the past month, trading just under its 50-day moving average of $265.02 on lighter-than-average volume of 25.8 million shares versus a 20-day average of 54.1 million. That leaves Apple in a consolidation band after a powerful run that pushed the company toward a $4 trillion market value in late 2025.[5]

Fundamentally, the backdrop remains tied to iPhone demand and the company’s push to turn its massive installed base into a recurring-revenue engine. On Jan 29, 2026, Apple projected 13% to 16% revenue growth for the March quarter, citing record iPhone results and signaling that hardware demand remains firm even as the broader smartphone market matures.[1] In Q4 2025, revenue reached $102.466 billion, up 7.94% year over year, with services revenue hitting a record $28.75 billion, underscoring how the higher-margin side of the business is doing more of the heavy lifting.[1]

Strategically, 2026 has been framed by some on Wall Street as Apple’s “year of AI,” with Wedbush arguing in February that a prior sell-off in the stock was “unwarranted” given the company’s positioning to roll out new AI features across its devices and services.[12] That AI narrative sits on top of the iPhone cycle and services growth, giving bulls multiple ways to justify a premium valuation even after the stock’s long run. Wedbush maintains a Buy rating and a $270 price target, which is only modestly above the current price and reflects expectations for “good headline numbers” as Apple continues to execute on its roadmap.[10]

Options traders have been active around these inflection points. In October 2025, as Apple hovered near record highs into earnings, one widely discussed strategy involved selling puts and buying calls to express a bullish view with defined risk, a structure that highlighted how many investors were willing to lean into upside while managing downside exposure.[9] That kind of positioning matters heading into a historically strong seasonal window, because it can amplify moves if the stock starts to trend and dealers adjust hedges.

Not every headline has been supportive. In August 2025, a former Louisiana attorney general launched an investigation into Apple’s officers and directors, adding a layer of legal uncertainty that has yet to translate into a clear financial impact.[13] Around the same time, some analysts argued that Apple’s surging free cash flow left the stock as much as 20% undervalued, reinforcing the idea that the company still had room to return capital and invest in new growth areas.[6] The tug-of-war between regulatory noise and cash-generation strength forms part of the backdrop as the seasonal window opens.

The chart below situates the latest move in its recent multi-month context.

Earnings and guidance context

Apple’s most recent reported quarter, covering Q4 2025, showed the company still has levers to pull even at its current scale. Revenue of $102.466 billion beat expectations, rising 7.94% from a year earlier, with earnings per share around $1.77 and services revenue at a record $28.75 billion.[1] Management’s guidance pointed to continued strength in iPhone sales and a supportive backdrop for the March quarter, where the company projected 13% to 16% revenue growth on the back of record device demand.[1]

Earlier in 2025, Apple had already demonstrated its ability to surprise on the upside. In July 2025, the company’s Q3 revenue beat estimates by nearly $5 billion, helping shares edge higher as investors recalibrated their expectations for the rest of the year.[3] A separate Reuters report that same day highlighted how Apple’s revenue forecast topped Wall Street estimates as iPhone sales soared, reinforcing the idea that the flagship product still has room to grow even in a mature market.[2]

On the qualitative side, Apple executives have repeatedly emphasized the importance of services, wearables and emerging AI features as drivers of future growth. The Q2 2025 earnings call in May 2025 focused heavily on how the company plans to deepen engagement across its ecosystem, from Apple TV+ to iCloud and Apple Music, in order to smooth out hardware cycles and build more predictable cash flows.[7] That strategy matters for the seasonal window because it can influence how investors react to any mid-window volatility: a strong services story can make it easier to look through short-term noise.

Macro and sector backdrop

Apple’s seasonal pattern does not exist in a vacuum. As one of the largest weights in the major U.S. equity indices, the stock often trades as a proxy for broader tech sentiment and risk appetite. In late 2025, Apple briefly reached a historic $4 trillion market capitalization, a milestone that underscored how tightly the company’s fortunes are tied to the direction of the overall market.[5] When Apple rallies, it can pull the S&P 500 and Nasdaq higher; when it stumbles, the drag can be just as pronounced.

Sector peers and macro conditions will shape how the upcoming window plays out. In November 2025, analysis of Apple’s free cash flow suggested the stock could be roughly 20% too cheap, even after a long bull run, because of the company’s ability to generate cash and return it to shareholders through buybacks and dividends.[6] That kind of argument tends to gain traction when interest rates stabilize and investors are willing to pay up for durable cash flows, especially in mega-cap tech.

At the same time, the legal and regulatory environment remains a wild card. The August 2025 investigation into Apple’s officers and directors highlighted how quickly governance questions can surface for large platforms.[13] While there has been no clear financial impact so far, any escalation during the seasonal window could test the historical pattern’s resilience.

Valuation and Street positioning

On valuation, Apple continues to command a premium multiple relative to many hardware peers, a gap that bulls justify with the company’s services mix, brand strength and balance sheet. In December 2025, one Forbes analysis laid out a path for how Apple stock could break $300, pointing to a combination of earnings growth, multiple expansion and continued buybacks as potential drivers.[14] With the shares currently trading in the low $260s, that kind of upside case remains in play if execution stays on track.

Sell-side sentiment is broadly constructive. Wedbush, which has been one of the more vocal bulls, reiterated its positive stance in July 2025, saying Apple was expected to report “good headline numbers” and flagging the upcoming iPhone 17 cycle as a key catalyst.[10] By February 2026, the firm was arguing that a prior sell-off was “unwarranted” and that 2026 could be Apple’s year of AI, as the company layers new capabilities onto its devices and services.[12] That backdrop of supportive analyst commentary feeds into how investors may interpret any pullbacks inside the seasonal window.

For a stock as widely owned as Apple, a 10-for-10 seasonal window with double-digit average gains is rare. The key question is not whether the pattern exists, but how investors choose to lean into it.

What to watch as the window opens

As Apple steps into this historically strong 232-day stretch, traders will be watching a handful of concrete markers. First, price behavior around the $265 area, which roughly lines up with the 50-day moving average, will show whether buyers are willing to defend the recent consolidation zone or wait for deeper pullbacks. A sustained break back toward the 52-week high near $288 would look more like the stronger years in the seasonal sample, where rallies built in stages and finished with double-digit gains.

Second, the next set of revenue updates will matter. The company has already guided to 13% to 16% growth for the March quarter on the back of record iPhone demand.[1] If actual results and forward commentary confirm that range, it would reinforce the fundamental backdrop that has historically supported this window. Any disappointment on iPhone or services growth, by contrast, could turn the usual mid-window consolidation into something sharper, even if the longer-term pattern remains intact.

Third, options and positioning deserve close attention. In October 2025, when Apple traded near record highs into earnings, one popular approach involved selling puts and buying calls to express a bullish view with controlled downside.[9] If similar structures reappear as the seasonal window progresses, it would signal that investors are again willing to lean into upside while managing risk, which can amplify directional moves as dealers hedge. A shift toward more defensive put buying without offsetting call demand would tell a different story.

Finally, watch how Apple trades on macro and regulatory headlines. The past decade’s 10-for-10 record includes years with significant drawdowns, including a 23.51% intraperiod slide in 2020 and double-digit setbacks in 2016, 2018 and 2022, before the stock ultimately finished higher. If the stock can absorb similar shocks in 2026 and still hold its longer-term uptrend, it would be another data point in favor of the seasonal pattern. If instead a negative catalyst breaks that rhythm, it will be a reminder that even the cleanest historical windows are tendencies, not guarantees.

Sources

- [1] Seeking Alpha: Apple projects 13%-16% revenue growth for March quarter as iPhone demand drives record results (Jan 30, 2026)

- [2] Reuters: Apple revenue forecast beats estimates as iPhone sales soar (Jul 31, 2025)

- [3] Seeking Alpha: Apple Q3 revenue crushes estimates by nearly $5B, shares edge higher (Jul 31, 2025)

- [5] Business Insider: Apple is reporting earnings today after reaching a historic $4 trillion market cap (Oct 30, 2025)

- [6] Barchart.com: Apple’s Free Cash Flow Surges, Implying AAPL Stock Could Be 20% Too Cheap (Nov 2, 2025)

- [7] Yahoo Finance: Q2 2025 Apple Inc Earnings Call (May 2, 2025)

- [9] CNBC: Apple gave up its earnings pop. How to trade it from here (Oct 31, 2025)

- [10] Seeking Alpha: Apple expected to report 'good headline numbers' says Wedbush (Jul 30, 2025)

- [12] Seeking Alpha: Apple sell-off 'unwarranted,' as Wedbush says 2026 is the tech giant's year of AI (Feb 17, 2026)

- [13] Morningstar: Apple investigation initiated by former Louisiana attorney general (Aug 16, 2025)

- [14] Forbes: How Apple Stock Can Break $300 (Dec 5, 2025)