Despite Solid Export Sales, Corn (CME) (ZC) Heads Toward Historically Weak 58-Day Summer Run

Corn (CME) is sitting near the middle of its 52-week range just days before a 58-day summer window that has delivered consistent downside in the past decade.

What is the seasonal pattern for Corn (CME) (ZC)?

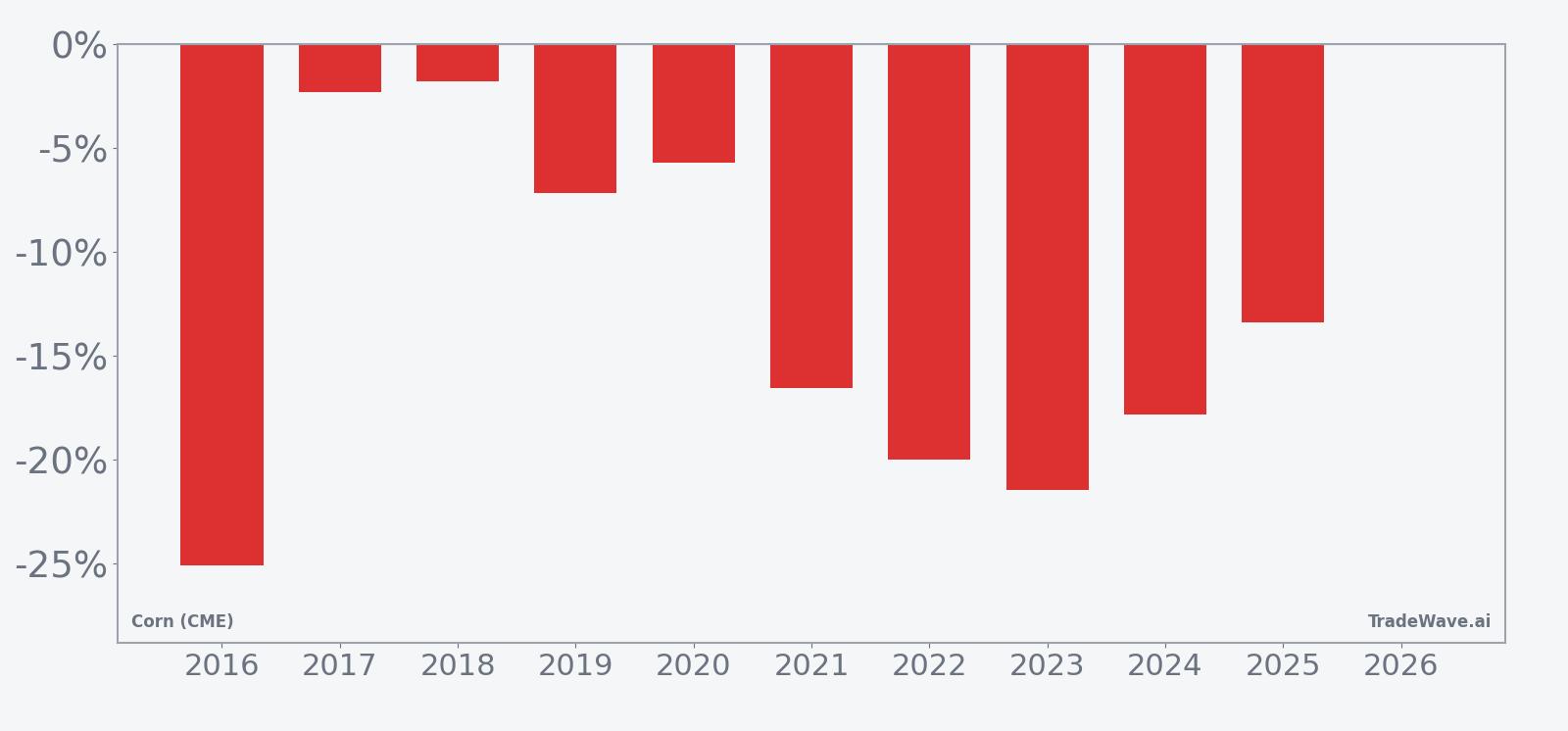

Corn (CME) has fallen in 10 of 10 years during this early-summer 58-day window, with an average gain of 13.12% for short positions in winning years.

- 10 for 10 in this window, with short trades averaging 13.12% profit across the past decade.

- Seasonal bias is bearish for futures prices from Jun 13 over the next 58 trading days.

- Percent Profitable is 100%, with 10 winners and 0 losers for the short-side pattern.

- Median profit for shorts is 14.96%, pointing to a consistently meaningful move when the pattern hits.

- TradeWave Ratio of 2.21 signals that price typically travels far in the trade direction within the window.

- Sharpe ratio of 1.5 indicates strong risk‑adjusted returns for the historical short setup.

According to historical data from TradeWave.ai, this upcoming stretch of the calendar has behaved very differently from an average month for corn futures. The next section walks through what that seasonal bias has looked like and how large the swings have been.

How has Corn (CME) (ZC) traded in this early-summer window?

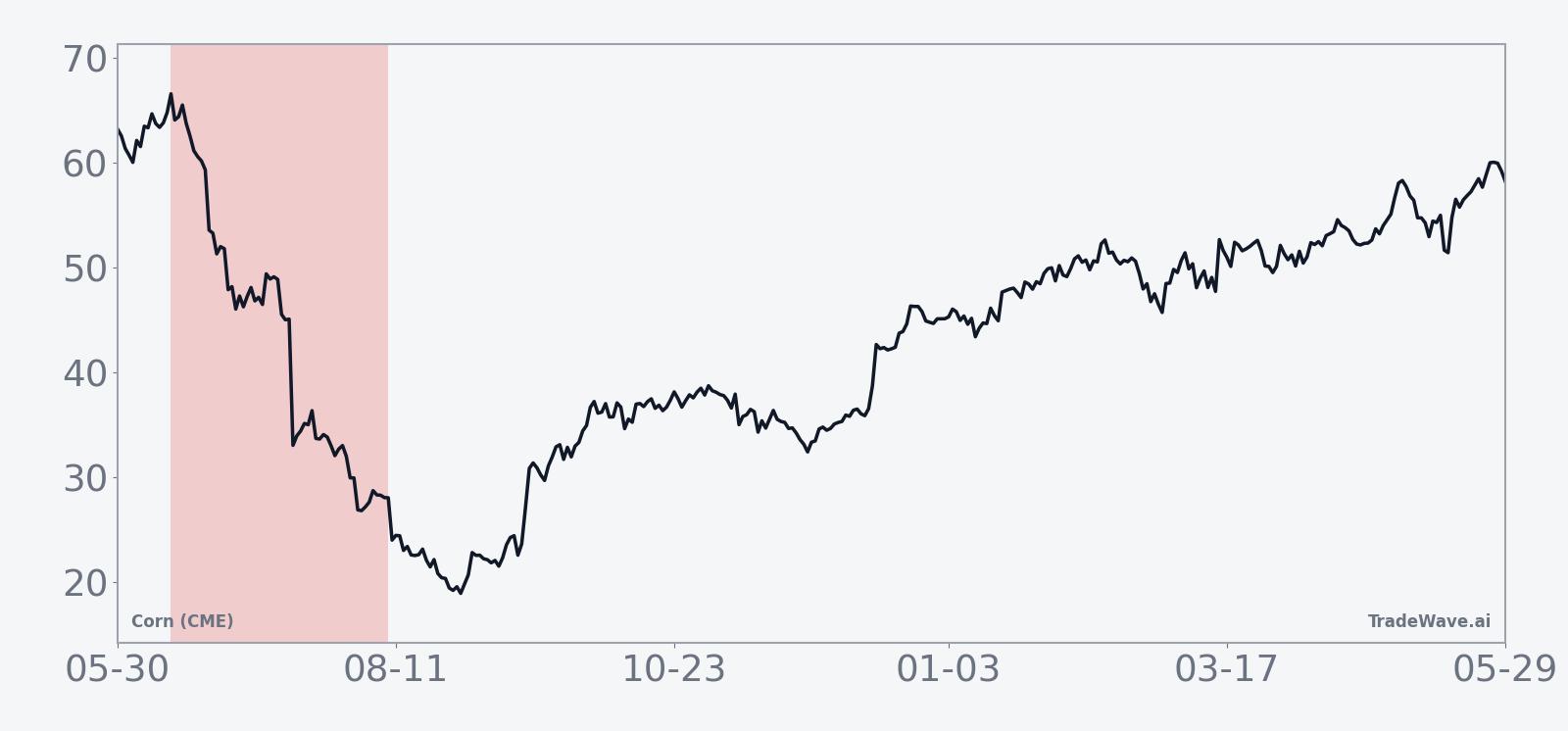

Corn (CME) has delivered profitable short trades in all 10 of the past years during the 58-day window that begins on Jun 13, with average gains of 13.12% for those short positions. Today the front-month contract settled at 423.0 cents per bushel, leaving it about 12.2% below its 52-week high of 481.75 and roughly 14.7% above its 52-week low of 368.75. That puts ZC squarely in the middle of its recent range as it heads toward a part of the calendar that has repeatedly rewarded traders betting on weaker prices.

Across the 10-year lookback, every iteration of this Corn (CME) trading window has ended with lower prices, which is why the pattern is classified as a short setup. The strongest year for shorts was 2016, when the contract dropped 25.06% between an entry around 430.0 and an exit near 322.25, while the softest outcome was 2018, which still produced a 1.8% decline from 376.0 to 369.25. Add it up: cumulative returns for the pattern total 234% over the decade, with a median profit of 14.96% for short positions.

The per-year path shows that these moves have not been gentle. In 2022, for example, corn futures fell 19.99% during the window, with the worst intraperiod drawdown from the entry level reaching 27.01% before the trade was closed. Even in milder years like 2017 and 2020, maximum adverse excursions still stretched to 6.5% and 6.68% respectively, underscoring that short positions have had to sit through meaningful volatility even when they ultimately paid off.

The 10-year average seasonal trend slopes steadily lower through most of the 58 days, with the bulk of the decline clustering in the middle of the window rather than at the start. That profile suggests that, historically, corn has tended to drift at first, then accelerate lower as the market digests early crop progress and supply signals. The cumulative return curve is relatively smooth, which is unusual for a commodity contract and speaks to how consistently this particular slice of the calendar has leaned in favor of shorts.

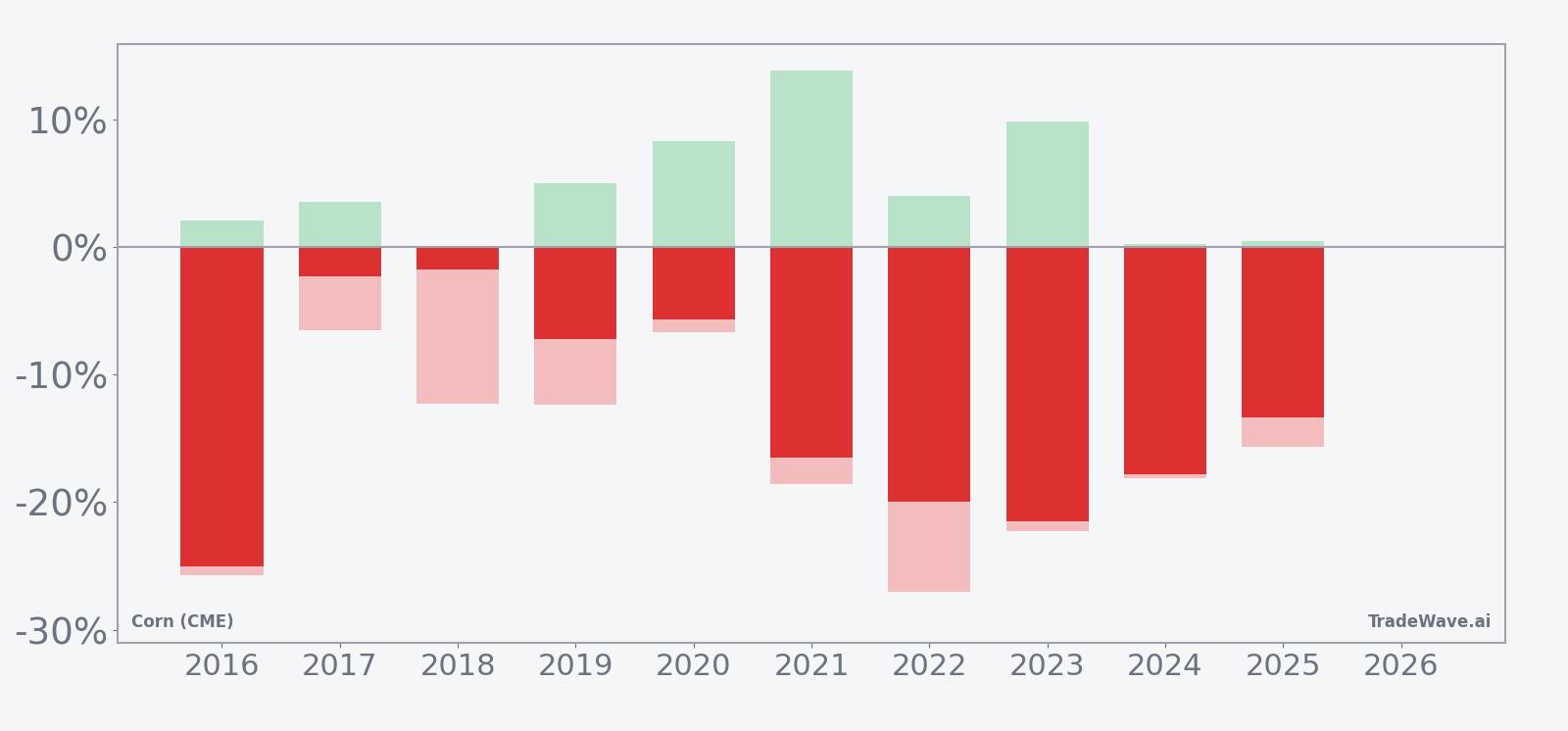

A second view that stacks yearly net returns with their best and worst intraperiod swings shows how far prices have tended to travel before the window closes.

The stacked net/MFE/MAE bars show that in big years like 2016, 2021, 2022 and 2023, short positions not only finished strongly profitable but also saw deep intraperiod drawdowns of 18% to 27% from the entry before the move was done. In contrast, years such as 2017 and 2018 had smaller net declines and more contained favorable excursions, but still ended in the green for shorts. The pattern is clear: this window has favored short exposure in 10 of 10 years, with sizable swings in both directions along the way.

History does not guarantee future results, and the worst intraperiod drawdowns (MAE) in this window have been large even in years that ultimately finished as winners for short positions.

Why does Corn (CME) (ZC) follow this seasonal pattern?

This early-summer stretch lines up with key points in the U.S. growing season, when planting is largely complete and early crop conditions start to firm up. One likely driver is that as weather risk becomes clearer and USDA supply estimates are updated, traders often shift from fear of tight supply toward more confidence in available stocks, which can pressure prices. The pattern may also reflect hedging flows from producers and merchandisers who lock in prices once they have better visibility on acreage and yield, adding selling pressure into this window.

What is driving Corn (CME) (ZC) today?

Corn futures ended Friday at 423.0 cents, down 0.18% on the day and roughly 6.41% lower over the past month, as the contract trades between its 52-week high of 481.75 and low of 368.75. The market is still digesting a heavier supply backdrop after the USDA raised U.S. corn ending stocks to 2.23 billion bushels in its January World Agricultural Supply and Demand Estimates, which boosted the 2025/2026 supply outlook and weighed on prices earlier in the year.[1]

At the same time, export demand has remained a stabilizing force. In late April, weekly USDA data showed net export sales of old-crop U.S. corn at 1,597,800 metric tons for the week ended Apr 23, a solid figure that helped reassure traders that global buyers are still active even as domestic stocks grow.[2] Higher oil prices have also supported the broader biofuel complex, tying corn more closely to energy markets as ethanol producers respond to shifting margins.[2]

The chart below situates the latest pullback in the context of the past year and overlays the upcoming seasonal projection.

What does the supply and demand backdrop mean for this window?

The seasonal pattern is unfolding against a backdrop of comfortable U.S. inventories. The USDA’s January report lifting ending stocks to 2.23 billion bushels signaled that supplies are more than adequate, which historically has made it harder for weather scares alone to sustain rallies.[1] When stocks are high, any improvement in crop conditions or modest demand disappointments can quickly translate into price pressure, especially in a window that has already leaned bearish for a decade.

On the demand side, the strong old-crop export sales reported for the week ended Apr 23 show that global buyers are still stepping in at lower price levels.[2] That demand helps cushion the downside but does not erase the impact of larger stocks, particularly if new-crop prospects remain favorable. For traders watching the ZC seasonal trend, the key question is whether export strength can offset the usual mid-season supply comfort that has historically weighed on prices in this 58-day stretch.

How are positioning and macro drivers interacting with the seasonal trend?

While detailed positioning data is not included here, the macro backdrop around corn is increasingly tied to energy markets. Higher oil prices tend to support ethanol margins and, by extension, corn demand for biofuel feedstock, which can blunt some of the seasonal downside when crude is strong.[2] Conversely, if oil softens into the window, the historical pattern of weaker corn prices could be amplified as both supply comfort and softer biofuel demand lean in the same direction.

For now, ZC is not stretched at either extreme of its 52-week range, which gives the upcoming seasonal window room to matter. If futures start the period near current levels and weather remains cooperative, the historical pattern suggests that rallies may have struggled to hold in prior years, with sellers reasserting control as the market gains confidence in the crop.

What should traders watch as this Corn (CME) (ZC) window opens?

Three things will be critical as the Jun 13 window begins. First, weekly USDA crop progress and condition reports will shape how quickly the market leans into the historical pattern; strong early readings have often coincided with the mid-window acceleration lower seen in the seasonal trend. Second, watch the 52-week band: sustained trade back toward 480 cents would signal that bulls are overpowering the usual early-summer softness, while a break toward the mid-300s would be more in line with the decade-long short-side record.

Third, keep an eye on the interaction between oil prices and corn demand for ethanol. If energy markets stay firm, that could provide a floor under ZC even as the seasonal window opens, while a pullback in crude would remove one of the few supports that has occasionally muted downside in prior years.[2] The historical pattern is strong, but how corn behaves against these macro and supply cues over the next 58 days will show whether this summer’s tape respects or challenges a 10-for-10 seasonal streak.

Sources

About this seasonal analysis

Seasonal pattern data is sourced from TradeWave.ai, which analyzes historical price behavior across annual calendar windows going back up to 30 years. Read the full data methodology or the book The 100-Year Pattern by Afshin Moshrefi (2026 edition). Past performance of seasonal patterns does not guarantee future results. This article is for informational purposes only and does not constitute investment advice.