Trust VIX Short-Term Futures ETF (VIXY) Has Fallen in 10 Straight Late-June Windows

Trust VIX Short-Term Futures ETF is sliding toward its 52-week low just as a 26-day late-June seasonal window that has seen VIXY fall in 10 straight years comes back onto the calendar.

What is the seasonal pattern for Trust VIX Short-Term Futures ETF (VIXY)?

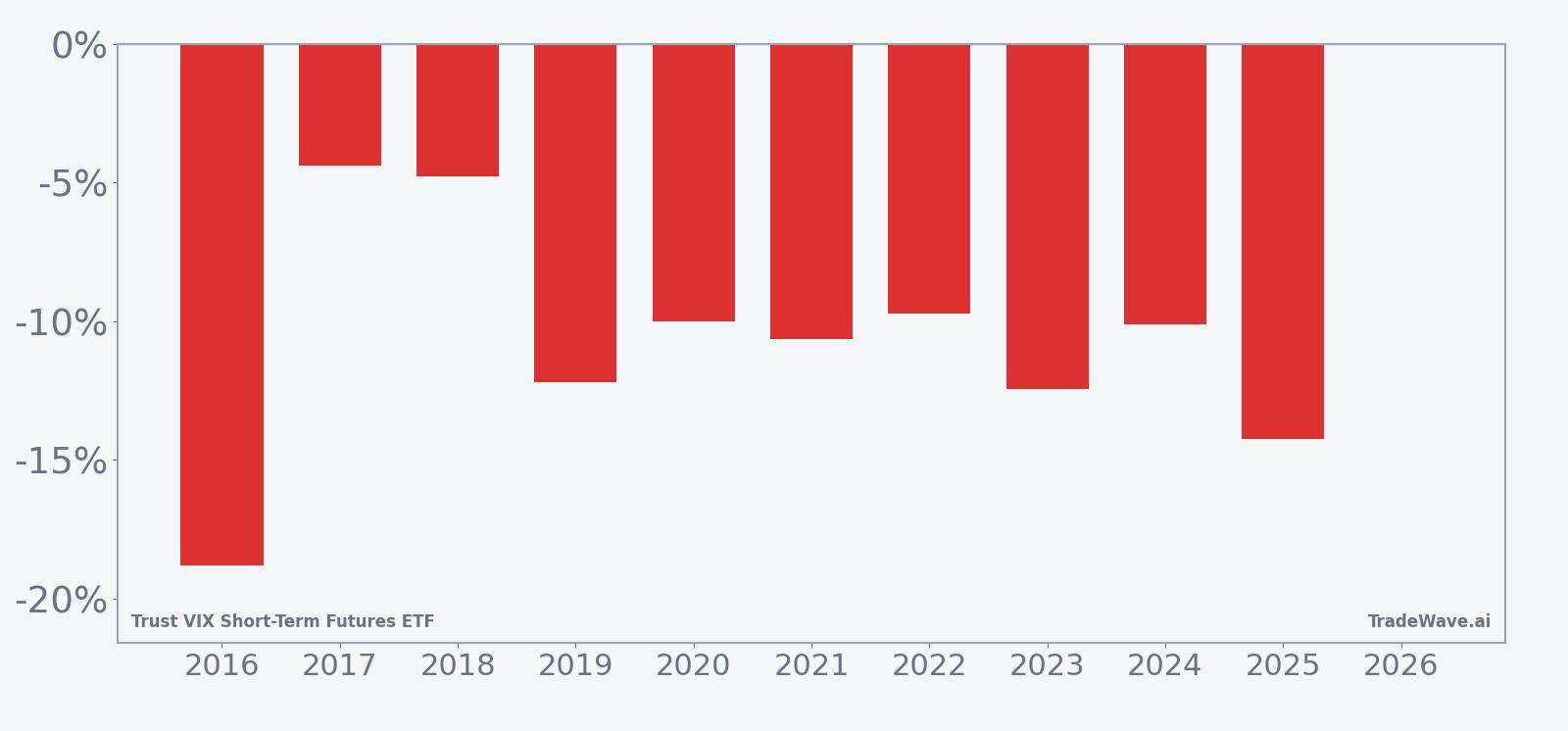

Trust VIX Short-Term Futures ETF has fallen in 10 of 10 years during this late-June 26-day window, with an average gain of 10.73% in winning short trades.

- 10 for 10 in this window, with short trades averaging 10.73% gains across the past decade.

- Seasonal window runs for 26 trading days starting Jun 19, covering the back half of June into mid-July.

- Percent Profitable is 100%, with 10 winners and 0 losers for the short-direction setup.

- Annualized return of 10.66% and a Sharpe ratio of 2.48 point to unusually consistent historical performance.

- TradeWave Ratio of 2.74 signals that VIXY has typically moved meaningfully in the short direction during this window.

- Individual years have still seen sizable intraperiod swings, so drawdowns against the short side can be sharp even when the final result is a win.

According to historical data from TradeWave.ai, this late-June stretch has behaved very differently from an average month for VIXY. The next section walks through how that pattern has played out over the past decade and what it means for volatility traders watching the calendar.

How has Trust VIX Short-Term Futures ETF (VIXY) traded in this late-June window?

Trust VIX Short-Term Futures ETF has declined in every single iteration of this 26-day late-June window over the past 10 years, with short positions averaging 10.73% gains. The next run of that window begins on Jun 19, just three days after VIXY closed at 21.75, about 60.2% below its 52-week high of 54.68 and only about 0.3% above its 52-week low of 21.68.[1] For a product built to spike when equity volatility erupts, that combination of depressed price and a historically bearish seasonal stretch for VIXY itself is hard to ignore.

Across the 10-year sample, every year shows a negative net return for VIXY in this window, which is a positive outcome for the short-direction pattern. The weakest year for VIXY was 2016, when the ETF fell 18.79% between entry and exit, while the smallest decline was 4.4% in 2017. Even in the milder years, the pattern has still delivered a meaningful drift lower in the product that tracks short-term VIX futures.

The average winner gain of 10.73% for shorts sits alongside a cumulative return of 175% across the decade, with an annualized return of 10.66%. That combination, plus a Sharpe ratio of 2.48, points to a window where the historical seasonality has not just been directional but also relatively smooth compared with many volatility-linked trades. For traders used to choppy VIX behavior, a 10-for-10 record with this kind of risk-adjusted profile stands out.

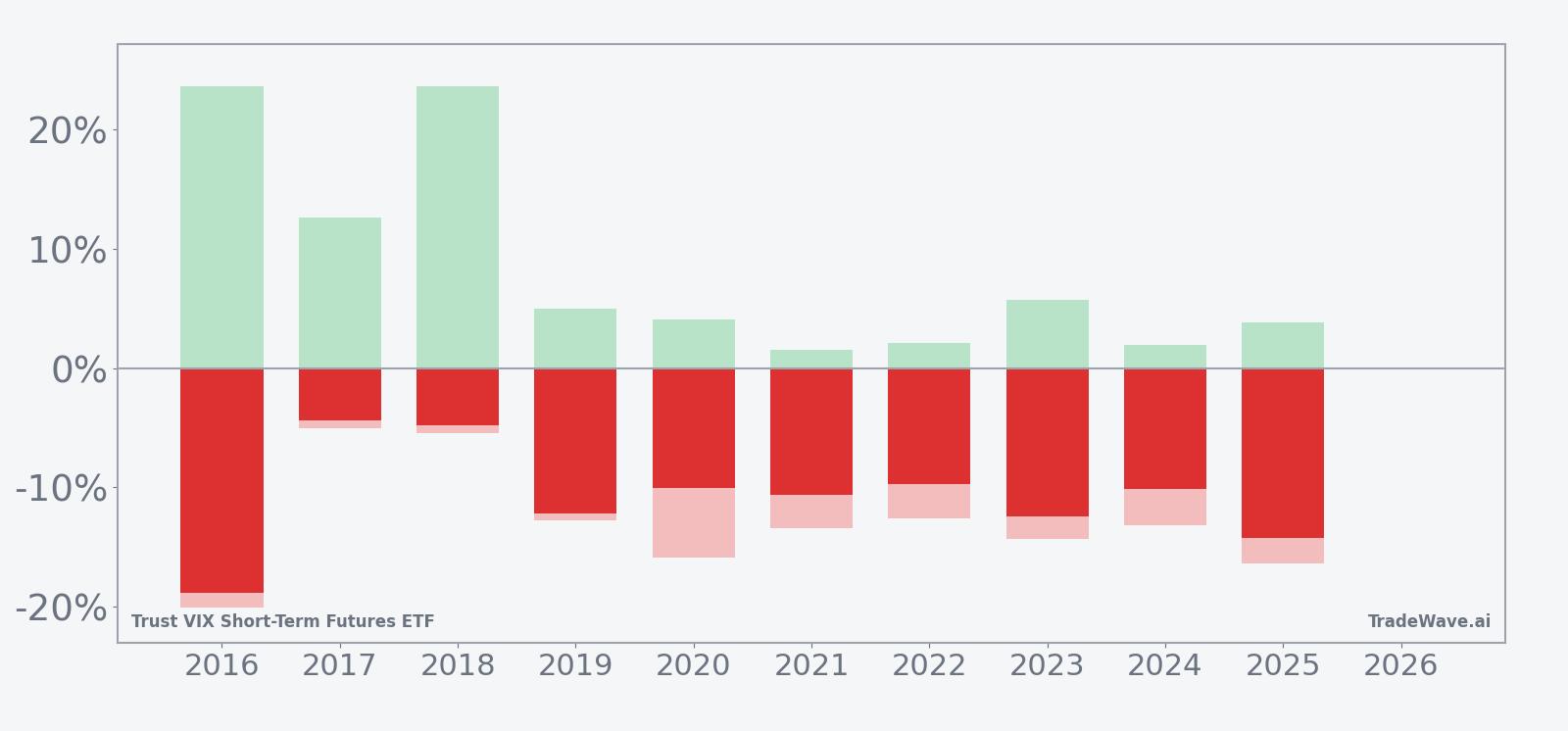

Intraperiod swings have still been large. In 2016 and 2018, for example, VIXY’s best point-to-peak moves against the short side reached 23.59% before the ETF ultimately finished the window sharply lower. In 2020, the worst drawdown from entry for shorts was 15.84% before the trade closed with a 10.02% gain. Those maximum favorable and adverse excursions show that even in a clean seasonal trend, volatility products can whip around violently inside the window.

The trend view of the 10-year seasonal average shows VIXY typically starting the window with a modest bounce or sideways action, then grinding lower into the back half of the period. That shape lines up with the per-year table, where several years saw early countertrend pops before the short side took control. For traders, the message is that patience has historically mattered more than perfect entry timing in this specific slice of the calendar.

A second view combines yearly net results with the best and worst intraperiod swings to show how far VIXY has tended to move inside the window.

Put together, the record is unusually clean for a volatility-linked ETF: 10 winners, no losers, and a consistent pattern of VIXY drifting lower across this late-June to mid-July stretch even when intraday and intraperiod swings were violent. The key takeaway is simple: over the past decade, this has been a window that has favored being short VIXY rather than long.

Why does Trust VIX Short-Term Futures ETF (VIXY) follow this seasonal pattern?

One likely driver is the way equity markets often stabilize into the early summer after spring macro and earnings catalysts, which can bleed premium out of short-term VIX futures. The pattern may also reflect institutional portfolio rebalancing and options expiration flows that tend to lean toward selling volatility as realized swings cool down. For VIXY, which holds a rolling basket of front-month VIX futures, that combination of calmer markets and negative roll yield has repeatedly translated into price pressure during this specific late-June window.

History does not guarantee future results; adverse excursions can be large even in winning windows, and volatility products like VIXY can move sharply against seasonal tendencies at any time.

What is driving Trust VIX Short-Term Futures ETF (VIXY) today?

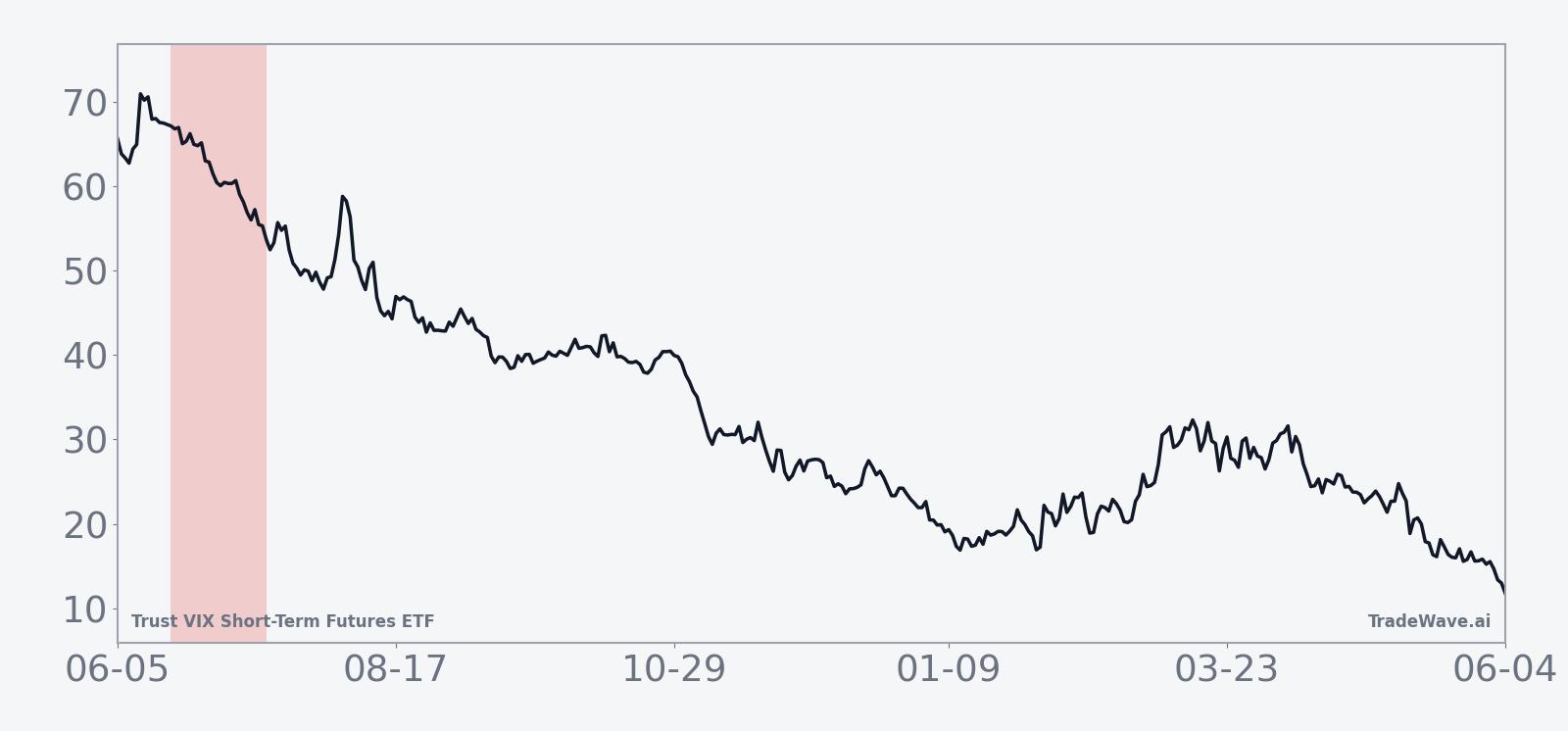

VIXY dropped 6.61% on Jun 16 to close at 21.75, extending a one-month slide of 19.42% and leaving the ETF just above its 52-week low of 21.68 and far below its 52-week high of 54.68.[1] Trading volume of about 2.49 million shares came in below the 20-day average of roughly 3.77 million, suggesting the latest leg lower has not yet attracted heavy new positioning.[1] With the 50-day moving average up at 26.73, VIXY is also trading well under a key trend gauge, underscoring how aggressively volatility has been sold in recent weeks.[1]

The chart below situates the latest move in its recent multi-month context and overlays the upcoming seasonal projection.

Because VIXY tracks short-term VIX futures rather than the spot VIX index, its path reflects both realized equity volatility and the shape of the VIX futures curve. When markets are calm and the curve is in contango, the ETF tends to bleed lower as it rolls from cheaper front-month contracts into more expensive second-month futures. That structural headwind has been on full display into mid-June, and the historical seasonality suggests that, at least in prior years, the pressure has often persisted through the next 26 trading days.

What should traders watch as this VIXY seasonal window opens?

For volatility traders, the first checkpoint is whether VIXY can hold above its 52-week low around 21.68 as the Jun 19 window begins, or whether another break lower confirms the historical pattern of late-June weakness.[1] The second is how realized equity volatility behaves around key macro and policy headlines; if stocks stay orderly and the VIX futures curve remains in contango, the backdrop will look similar to prior years when VIXY drifted lower through this stretch. Finally, watch the relationship between VIXY and its 50-day moving average: in past cycles, sustained trading below that line during this window has often coincided with the strongest short-side outcomes. If volatility spikes and VIXY rips back above that trend marker instead, it would be an early sign that this year’s late-June pattern may diverge from the last decade’s script.

Sources

About this seasonal analysis

Seasonal pattern data is sourced from TradeWave.ai, which analyzes historical price behavior across annual calendar windows going back up to 30 years. Read the full data methodology or the book The 100-Year Pattern by Afshin Moshrefi (2026 edition). Past performance of seasonal patterns does not guarantee future results. This article is for informational purposes only and does not constitute investment advice.