Dollar Tree (DLTR) Has Rallied 10 Straight Years in This 7-Day March Window

Dollar Tree is approaching a short March stretch that has delivered gains in every year of the past decade, just as the stock trades well below its 52-week high and management turns cautious on sales growth.

Key takeaways

- Dollar Tree’s 7-day window starting Mar 23 has been positive in 10 of 10 years, a 100% hit rate for long setups.

- Average gain across those winning years is 4.71%, with cumulative returns of 58% over the decade.

- The pattern is long-biased, with a TradeWave Ratio of 2.08 and a Sharpe ratio of 2.43, pointing to historically strong risk-adjusted upside.

- Intraperiod swings have been manageable in most years, but 2025 saw a sharp drawdown before finishing higher, showing that adverse moves can still bite.

- The window opens as DLTR trades about 25.9% below its 52-week high and management guides to slower sales growth amid tariff and freight uncertainty.[5]

According to historical data from TradeWave.ai, this upcoming stretch has behaved very differently from an average week on the calendar for Dollar Tree. The next section looks at how that pattern has played out over the past decade and what it means for the days ahead.

Seasonal window

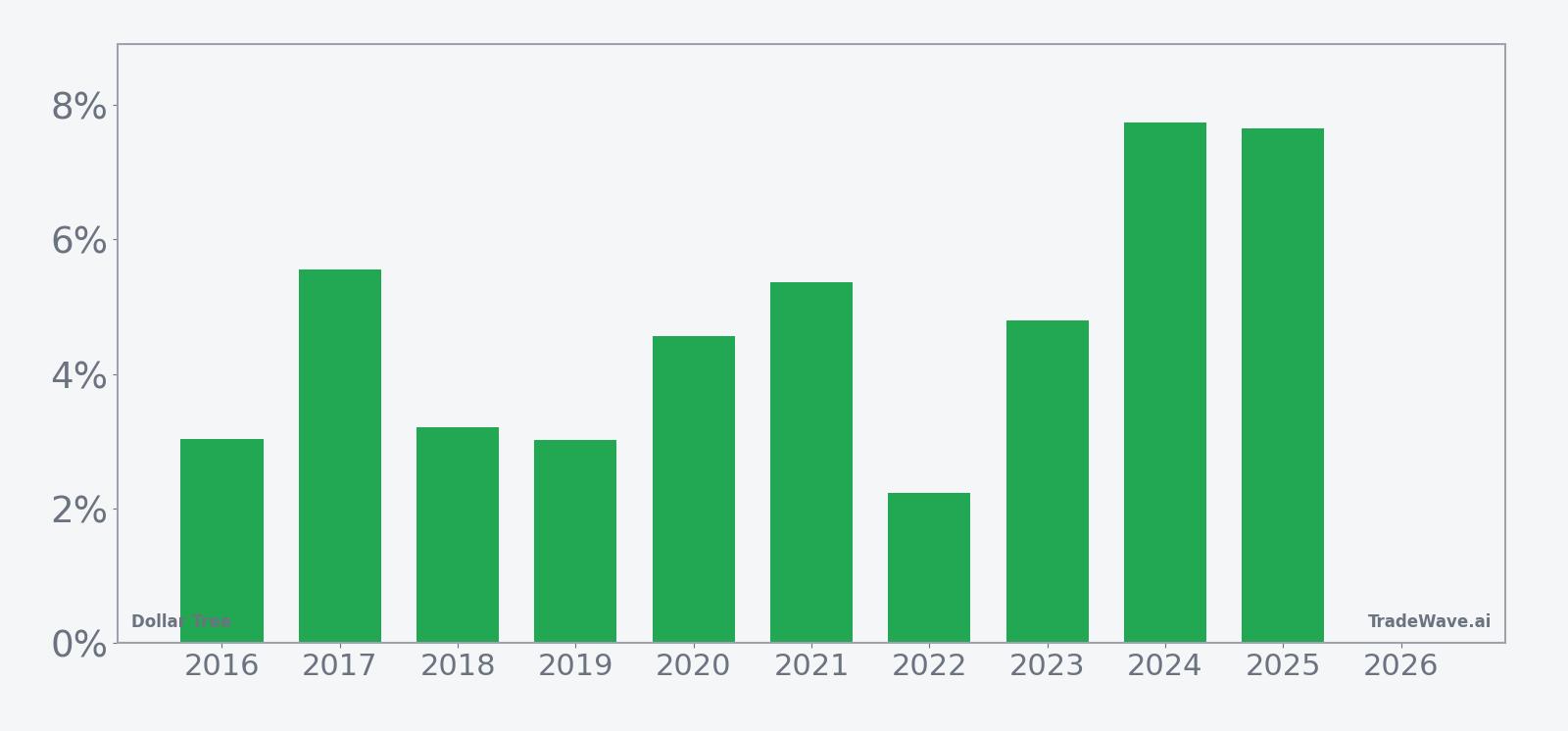

Dollar Tree has posted gains in this late-March 7-day window in 10 of the past 10 years, with average profits of 4.71% for long trades. The next iteration begins on Mar 23, with the stock last changing hands at $105.56 on Friday, about 25.9% below its 52-week high of $142.40 and well above its 52-week low of $61.87. That combination of a clean historical win streak and a stock trading at a discount to its recent peak gives this short window unusual weight on the calendar.

The 10-year average trend line for this window slopes steadily higher, with most of the typical gain accruing across the full week rather than in a single spike. That fits a profile where long trades have tended to work consistently, not just off one or two outlier years.

A closer look at yearly net returns and intraperiod swings shows how upside and downside have traded off inside the window.

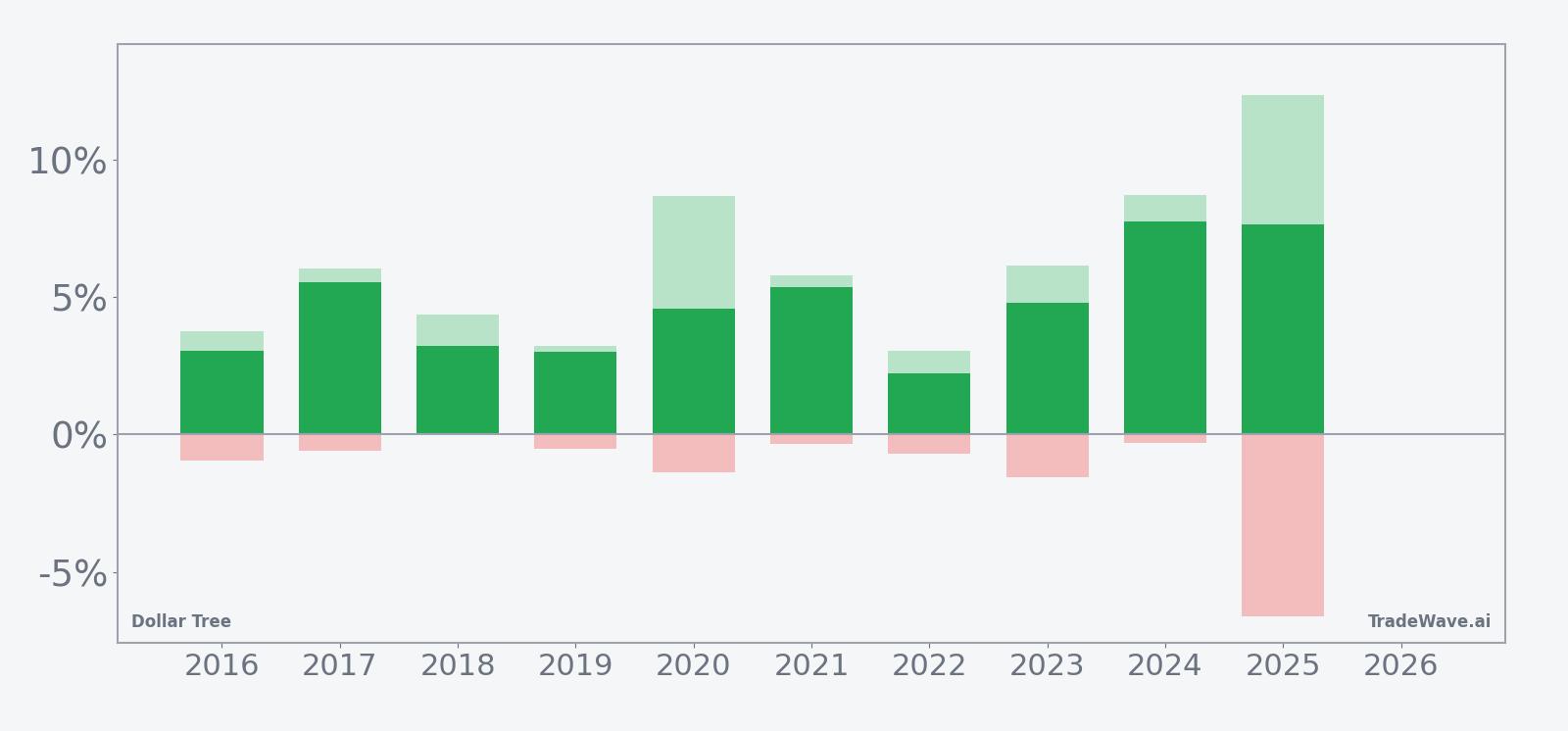

Across the decade, average winners gained 4.71%, while the strongest years, such as 2024 and 2025, posted net returns of 7.74% and 7.64% respectively. Maximum favorable excursions, the best point-to-peak moves inside the window, have reached as high as 12.35% in 2025, showing that when the pattern runs, it can run hard. On the downside, maximum adverse excursions, the worst drawdowns from entry, have usually been contained to low single digits, although 2025 saw an intraperiod drop of 6.6% before finishing higher, a reminder that even “all green” windows can be bumpy.

Year by year, the weakest outcome in this sample was still a gain of 2.23% in 2022, while the strongest was 7.74% in 2024. The consistency is striking: 10 winners, zero losers, and a Sharpe ratio of 2.43 for this specific slice of the calendar. Add it up and the cumulative return across these ten late-March windows is 58%, all aligned with a long trade direction.

History does not guarantee future results; even in windows with perfect win records, adverse excursions can be large enough to challenge positions before any upside plays out.

Price and near-term drivers

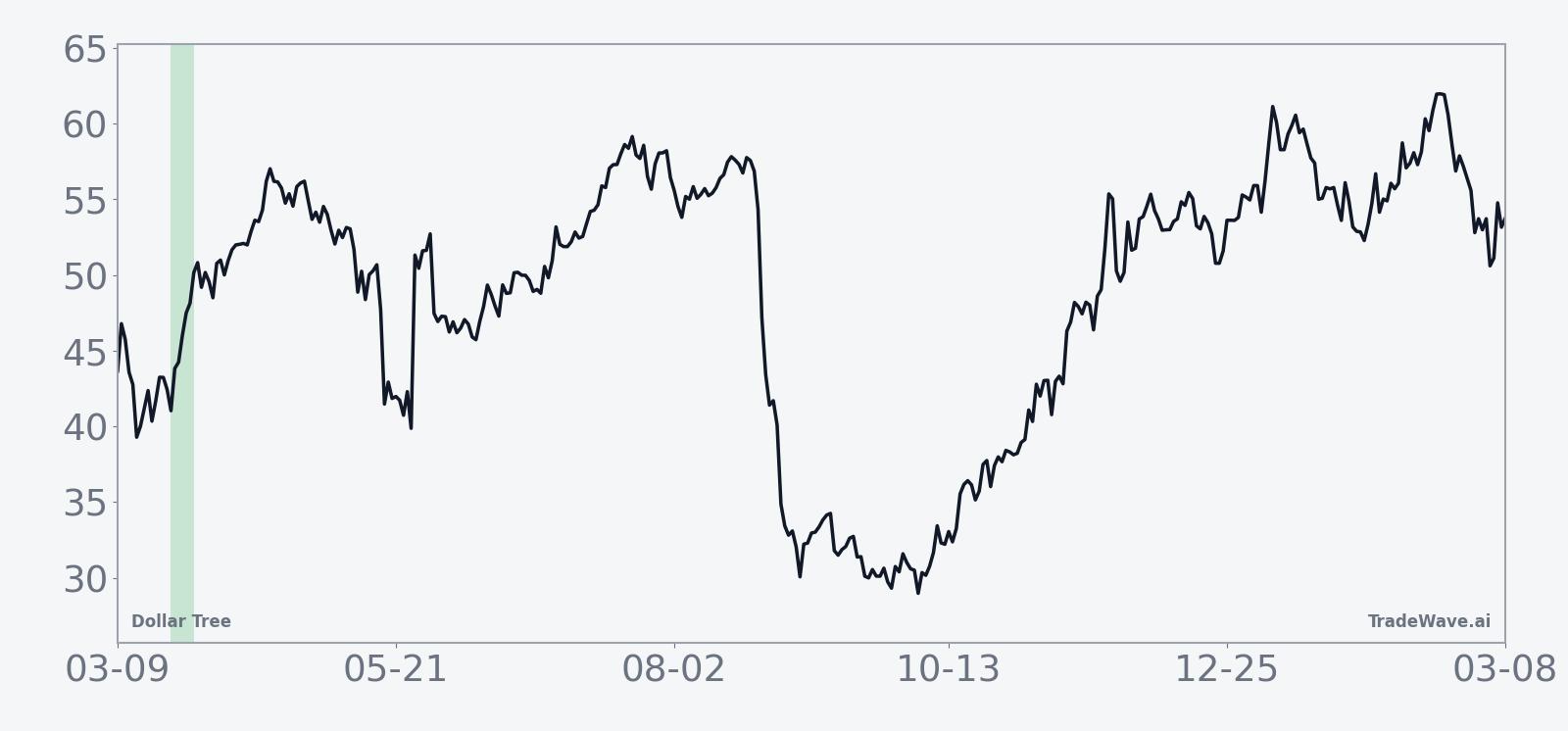

Dollar Tree shares closed Friday at $105.56, down 1.8% on the day and well below the 50-day moving average of $124.14. The stock has dropped 21.0% over the past month, leaving it sharply off its 52-week high of $142.40 but still far above the 52-week low of $61.87, with trading volume over the last 20 days averaging about 3.0 million shares.

On Mar 16, Dollar Tree told investors it expects sales growth to slow in 2026 as tariffs and freight costs weigh on margins, even as demand for discretionary products remains solid.[5] That cautious tone follows a period in which the company had raised its annual earnings forecast and leaned into a multi-price strategy to boost per-unit margins and broaden its customer base, a shift that has helped drive sales but also added complexity to the model.[3] In June 2025, the company also warned that second-quarter profit could fall by about 50% because of tariff pressure and the planned sale of Family Dollar, underscoring how exposed the business is to policy and logistics shocks.[3]

Competitive pressure is another overhang. In October 2025, Jefferies downgraded Dollar Tree to underperform, arguing that operational complexity and intensifying rivalry from chains like Dollar General and Walmart were eroding its differentiation and raising execution risk.[1] In December 2025, a separate analysis highlighted that Dollar Tree’s stock had already surged about 70% from earlier lows, raising questions about how much of the turnaround and pricing strategy shift was already reflected in the share price.[4]

The chart below situates the latest pullback against Dollar Tree’s past year of trading.

Earnings and guidance backdrop

Dollar Tree’s most recent reported quarter delivered $10.65 billion in net sales, ahead of estimates, with earnings per share of $1.28 versus expectations of $0.95.[3] Traffic has started to decelerate and spend per trip has turned negative, a sign that even value-focused shoppers are becoming more cautious on basket size.

The company has raised its full-year earnings forecast to a range of $6.30 to $6.50 per share and is targeting same-store sales growth of 2.5% to 2.7%.[3] At the same time, management has flagged that second-quarter profit could be cut in half by tariffs, a warning that sits uncomfortably alongside the upbeat seasonal pattern for the stock. The next formal earnings date has not yet been set, but the calendar suggests investors will be trading this late-March window with fresh guidance from earlier in the month still in mind.

Macro and sector context

Tariff uncertainty remains a central macro risk for Dollar Tree. Higher import costs and shifting trade policy have already pressured profitability and forced the company to rethink pricing and assortment, leaving it more exposed to external shocks than many investors might assume.[3] Freight costs add another layer of volatility, particularly for a chain that relies on high volumes of low-ticket items to make the math work.

On the sector side, discount retail is as competitive as it has ever been. Dollar Tree is fighting for share against Dollar General and big-box players like Walmart, which have leaned into value messaging as inflation-weary shoppers trade down.[1] In December 2025, rivals were still able to raise profit forecasts on resilient demand for essentials, highlighting how execution and mix decisions can separate winners from laggards even inside the same macro backdrop.[2]

Valuation and the Street view

Analysts are split on how to balance Dollar Tree’s strategic changes with its execution and macro risks. Jefferies carries a Hold-equivalent stance with a cited consensus price target of $70, a level that sits far below the current $105 handle and reflects an earlier, more cautious price regime rather than today’s tape.[1] That disconnect between the stock and at least one published target underlines how quickly sentiment has swung over the past year as the company’s multi-price strategy and profit guidance evolved.

For traders watching the upcoming seasonal window, the key question is not whether the stock is “cheap” or “expensive” on traditional metrics, but how a historically strong short-term pattern interacts with a market that has already repriced the name aggressively off its lows.

What to watch as the window opens

The 7-day window starting Mar 23 has a rare profile for a single-stock pattern: 10 winners, zero losers, and average gains north of 4% for long trades. The stock is entering that stretch after a sharp one-month slide and under a cloud of tariff and freight uncertainty, which means any upside follow-through will be trading against a cautious fundamental narrative rather than riding a wave of optimism.[3][5]

Into and through this window, traders will be watching a few key markers. First, whether Dollar Tree can reclaim and hold levels above the 50-day moving average near $124 would say a lot about how much of the recent guidance reset is already priced in. Second, intraday behavior will matter: a pattern of early-week drawdowns followed by strong closes would rhyme with prior years where maximum adverse moves were followed by solid net gains. Third, any fresh commentary on tariffs, freight costs or the Family Dollar sale could either reinforce or undercut the seasonal tailwind, especially if it shifts expectations for that projected 50% second-quarter profit hit.[3][5]

History shows this late-March stretch has been kind to Dollar Tree bulls. The next few sessions will test whether that decade-long record can withstand a tougher macro and competitive backdrop than many of those prior years faced.

Sources

- CNBC, "Dollar Tree gets a downgrade from Jefferies as discount retailer struggles versus competitors" (Oct 7, 2025)

- Reuters, "Dollar General raises annual profit forecast on resilient demand for essentials" (Dec 4, 2025)

- Reuters, "Dollar Tree forecasts weak second-quarter profit on tariff uncertainty" (Jun 4, 2025)

- Forbes, "What's Next After A 70% Surge In Dollar Tree Stock?" (Dec 9, 2025)

- Wall Street Journal, "Dollar Tree Sees Sales Growth Slowing Despite Influx of Inflation-Weary Shoppers" (Mar 16, 2026)