FNB Corporation (FNB) Has Dropped in All 7 Midterm Spring Windows as 120-Day Weak Stretch Nears

FNB Corporation is approaching a 120-day midterm-election-year stretch that has been consistently weak for the stock, even as shares trade well below their 52-week high.

Key takeaways

- FNB Corporation has posted losses in all 7 midterm-election-year spring windows in this study, aligning with a short trade direction.

- The upcoming 120-day window begins Mar 20, 2026 and runs through mid-July, covering the heart of the midterm-year policy debate.

- Across those seven cycles, the average profit for the short setup is 6.61%, with a cumulative return of 56% for the strategy.

- Every year in the sample was a winner for the short, with 7 winners and 0 losers and a Sharpe ratio of 1.48.

- Intraperiod swings have been sharp, with several years showing double-digit peak drawdowns against the trade before finishing lower.

- FNB shares closed at 15.83 on Mar 18, about 17.3% below their 52-week high of 19.14, after a 12.78% slide over the past month.

According to historical data from TradeWave.ai, this specific midterm-election-year stretch has behaved very differently from an average quarter for FNB Corporation, and the next iteration starts tomorrow.

Seasonal window

FNB Corporation has fallen in all 7 midterm-election-year windows that start around Mar 20 and run for 120 trading days, with an average short-side gain of 6.61%. Shares finished Wednesday at 15.83, down 1.7% on the day and about 17.3% below the 52-week high of 19.14, after a 12.78% drop over the past month.[1]

This window begins on Mar 20, 2026 and spans 120 trading days, covering the last 7 midterm election years in the dataset. Grouping by the presidential cycle matters because regional banks like FNB tend to feel policy shifts in regulation, capital standards and the rate path most acutely during mid-cycle debates, when Congress and regulators revisit post-crisis rules and funding priorities.

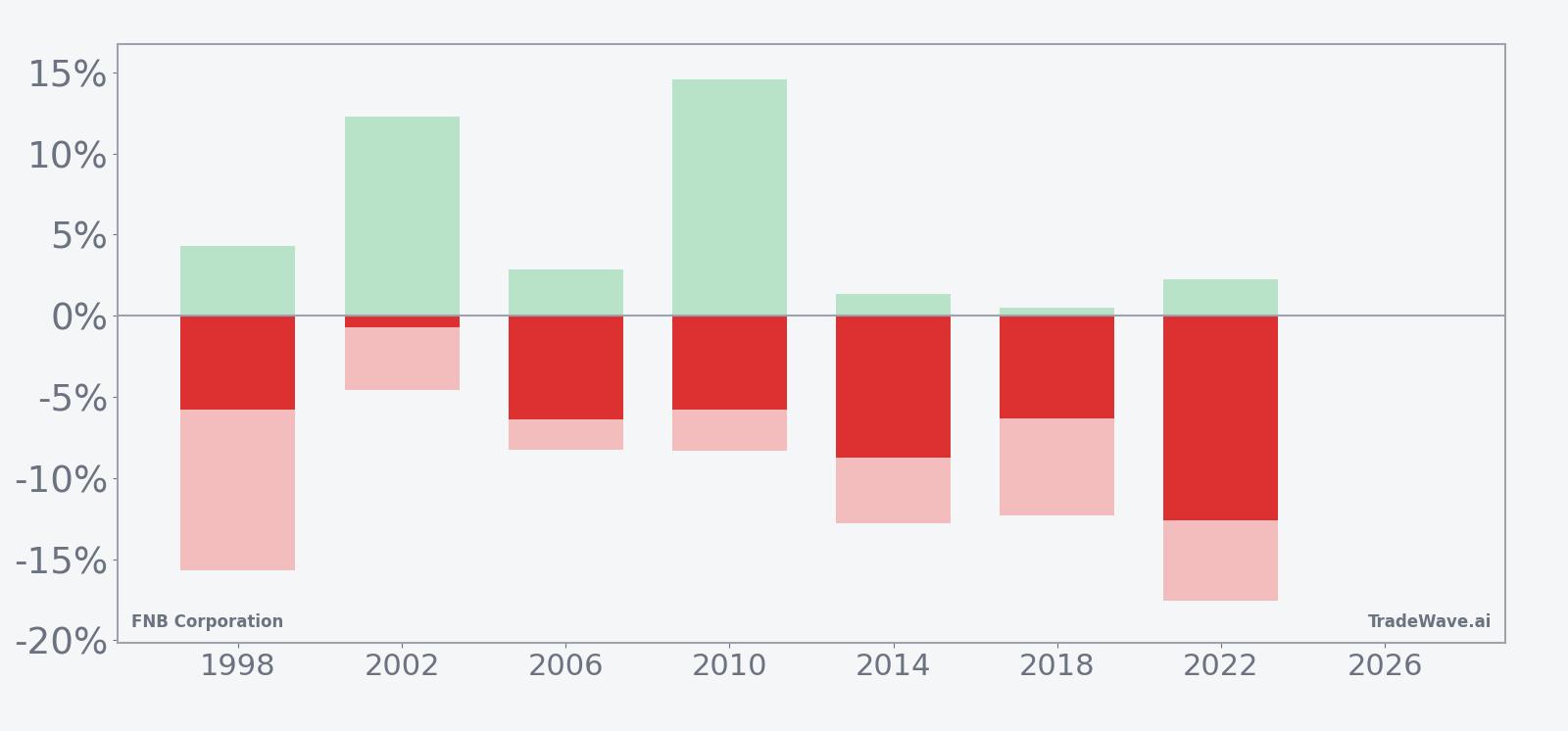

The trade direction for this pattern is short. In every one of the seven midterm-year windows since 1998, a short position entered at the start and held for the full 120 days would have finished profitable, with 7 winners and 0 losers. The average profit across those winning years is 6.61%, and because there were no losing years in the sample, the all-years average matches that figure.

Individual years show how that has played out. In 1998, a short entered at 4.69 and exited at 4.42 produced a 5.77% gain for the trade, while 2014 delivered an 8.73% gain as the stock fell from 8.60 to 7.85 over the window. The most favorable year for the short was 2022, when FNB dropped 12.6% from 11.24 to 9.83 during the same midterm-year stretch.

Intraperiod swings have been meaningful. The best point-to-peak move in favor of the short, known as the maximum favorable excursion, reached 14.57% in 2010, while several years saw favorable moves in the low-to-mid teens. At the same time, the worst drawdowns from entry, or maximum adverse excursions, have also been large, with years like 1998 and 2014 showing adverse moves of 15.71% and 12.81% respectively before the trade ultimately finished in the money.

The TradeWave Ratio (TWR) for this pattern is 2.19, which measures how far price typically travels in the trade direction within the window, independent of the final close. A Sharpe ratio of 1.48 indicates that, based on end-of-window outcomes, the risk-adjusted returns for this short setup have been relatively strong compared with many single-stock seasonal patterns.

Looking at the historical seasonal trend, the average path for FNB in these midterm-year windows shows a tendency for weakness to build gradually rather than in a single air pocket. The seasonal curve slopes lower over the 120 days, with some choppy stretches but no persistent rallies that fully erase the downtrend.

Year-by-year bars with peak favorable and adverse moves show how consistently the short has worked, and how bumpy the ride has been.

Put together, the pattern is unusually one-sided: seven for seven winning short windows, meaningful average gains and a history of sizable intraperiod swings that have still resolved lower by the end of the period. History does not guarantee a repeat, but this is one of the cleaner midterm-year short regimes in the FNB seasonal playbook.

History does not guarantee future results, and the worst intraperiod drawdowns have been large even in years that ultimately finished profitable for the short.

Price and near-term drivers

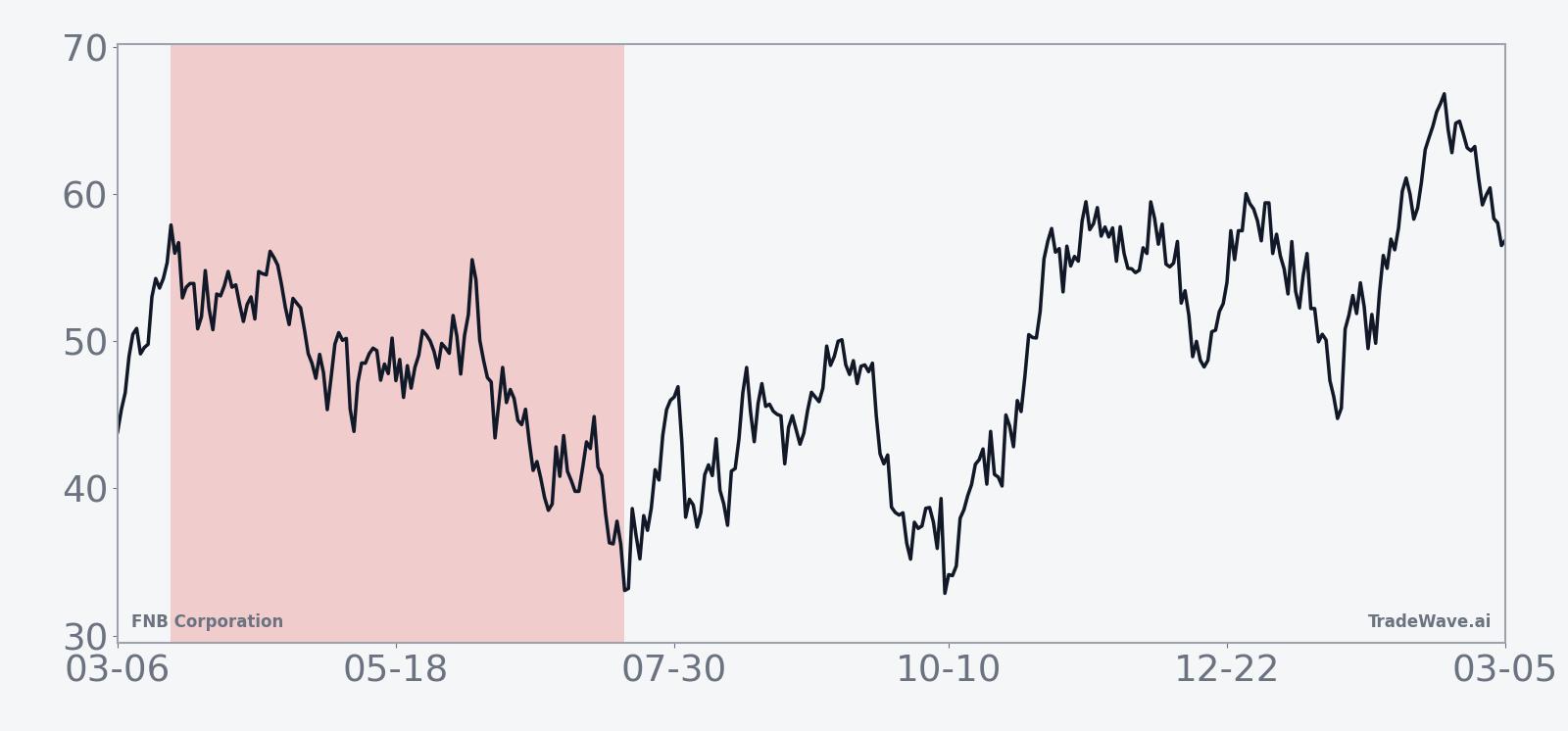

FNB shares closed at 15.83 on Mar 18, down 1.7% on the session, extending a one-month slide of 12.78% that has pulled the stock about 17.3% below its 52-week high of 19.14.[1] Trading volume over the past 20 days has averaged roughly 8.45 million shares, so Wednesday’s 6.57 million turnover landed slightly below recent norms as the stock drifted lower.[1]

That price action leaves FNB below its 50-day moving average of 17.45, a sign that the near-term trend has rolled over after a stronger stretch earlier in the year.[1] With no near-term earnings date or major company-specific catalysts flagged in public calendars, the stock is trading more as a macro and rates proxy for regional banks than on idiosyncratic news.

The chart below situates the latest move in its recent multi-month context.

Macro and election-cycle backdrop

The upcoming window sits in the early part of the midterm election year, a phase that often brings renewed focus on bank regulation, capital rules and the path of interest rates. For regional lenders, that mix can translate into choppy trading as investors handicap how far policymakers will go on capital buffers and how quickly the Federal Reserve might adjust policy in response to growth and inflation data.

In prior midterm years, the first half of the year has often been the more volatile stretch for financials, with policy debates and committee hearings front-loaded before campaigns fully ramp. For a name like FNB, which is sensitive to both net interest margins and credit quality expectations, that has historically lined up with the 120-day window that starts in late March.

What to watch as this window opens

As the 2026 midterm-year window begins on Mar 20, traders will be watching whether FNB’s recent weakness continues to track the historical pattern or stabilizes despite the seasonal headwind. A sustained break below the recent lows on rising volume would look more like prior midterm-year windows that delivered double-digit short-side gains, while a quick reclaim of the 50-day moving average would mark a departure from the typical path.

Policy and macro headlines will matter. Any shift in expectations for the Fed’s rate path, or fresh signals on regional bank oversight from regulators and lawmakers, could either reinforce or blunt the historical tendency for FNB to drift lower in this part of the cycle. The key tell inside the window will be how the stock behaves on those news days: in past midterm years, rallies have tended to fade over the following weeks rather than launch new uptrends.

For this specific 120-day stretch, the historical record suggests three practical checkpoints. First, how FNB trades in the first month of the window, when prior years have sometimes seen early adverse moves against the short before the trend reasserted. Second, whether any mid-window bounce can push the stock back toward the 52-week high zone near 19, which would be unusual relative to the last seven cycles. Third, how the stock behaves into the final weeks of the window, when prior midterm years have often seen the downtrend flatten but not fully reverse.

If FNB manages to hold above recent lows and rebuild momentum despite this historically weak midterm-year window, it would mark a clear break from the seven-for-seven short track record. If instead the stock continues to leak lower on macro and policy noise, the 2026 iteration could end up looking a lot like its predecessors.