Devon Energy (DVN) Has Rallied in 8 of 9 Midterm Spring Windows, and the Next One Is Opening

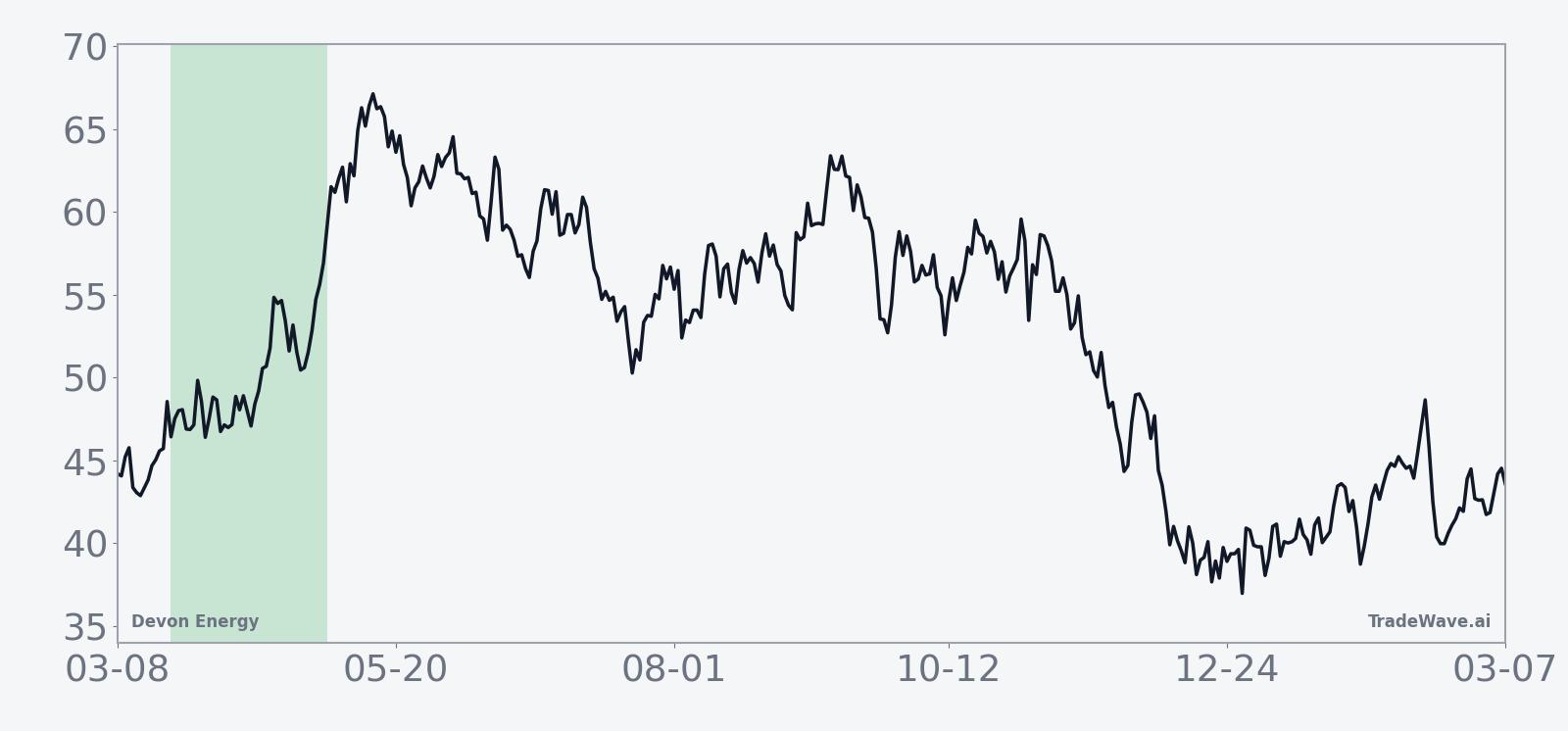

Devon Energy is trading just below a fresh 52-week high as it heads into a historically strong 42-day midterm-year spring stretch that has often rewarded long exposure.

Key takeaways

- Devon Energy’s upcoming 42-day window starting Mar 22 in midterm election years has been positive in 8 of 9 cycles, or 89% of the time.

- Winning years in this window have averaged gains of 7.7%, while including the lone losing year brings the all-years average to 6%.

- The pattern is long-biased, with a Trade Direction of “long” and a TradeWave Ratio of 1.65, pointing to meaningful historical travel in the upside direction.

- Intraperiod swings have been real: the weakest year saw a drawdown of 12.39% from entry even though the overall sample is strongly positive.

- DVN closed at 47.42 on Mar 18, about 0.2% below its 52-week high of 47.50, after announcing a $58 billion all-stock merger with Coterra in February.[1][4]

- History does not guarantee a repeat, but the combination of a strong midterm-year pattern and a stock sitting near its highs gives this window extra focus.

According to historical data from TradeWave.ai, this specific midterm-year spring stretch has behaved very differently from an average month for Devon Energy, and the next iteration is about to open.

Seasonal window

Devon Energy has risen in 8 of the last 9 midterm election years during this 42-day spring window, averaging 7.7% gains in the winning runs. The next window begins on Mar 22, with the stock sitting at 47.42, about 0.2% below its 52-week high of 47.50.[1] That puts a historically bullish seasonal pattern right on top of a stock that has already been grinding higher into the midterm election year.

The presidential election cycle matters here because this pattern only looks at the last nine midterm election years, not every single year on the calendar. Midterm years often bring policy noise, shifting expectations for regulation and spending, and choppy tape for cyclicals, yet this particular slice of the calendar has tended to favor Devon bulls.

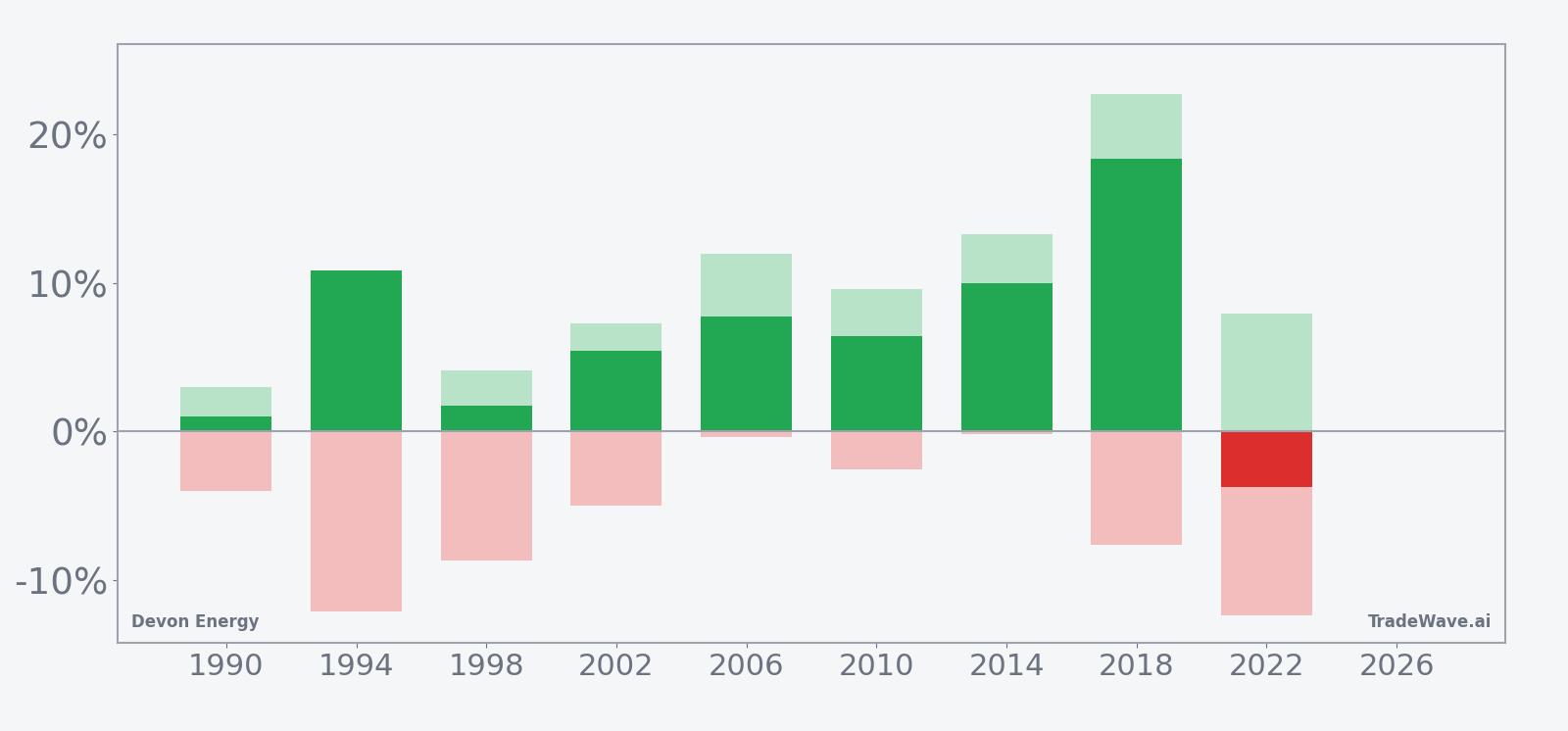

Across the nine midterm-year samples, the long-bias is clear. Percent Profitable sits at 89%, with 8 winners against just 1 loser, and the all-years average outcome of 6% suggests that even when the lone down year is included, the window has still skewed positive for long positions. The median profit of 6.45% lines up closely with that average, which points to a fairly consistent upside profile rather than one or two outlier years doing all the work.

Looking at individual years, 2018 stands out as the strongest run, with an 18.4% net gain and a maximum favorable move of 22.7% from entry before the window closed. On the other side of the ledger, 2022 is the only losing year, with a net decline of 3.76% and a maximum adverse move of 12.39% from the starting point, a reminder that even in a strong pattern, drawdowns can bite.

The historical seasonal trend line for this window shows gains tending to build steadily rather than in a single burst. In many years, the typical pattern has been a firm start, a mid-window pause or shallow pullback, and then another push higher into the back half of the 42 days.

The next chart layers yearly net results with the best and worst intraperiod swings to show how far DVN has tended to travel inside the window.

The stacked bar view of net results, maximum favorable moves and maximum drawdowns shows why this window commands respect. In most years, the maximum favorable excursion has been meaningfully larger than the final net gain, which lines up with a TradeWave Ratio of 1.65 and suggests that intraperiod rallies have often overshot the eventual close. At the same time, several years, including 1994, 1998 and 2022, saw adverse moves of 8% to more than 12% from entry, underscoring that even a strong long-biased window can involve sharp pullbacks before finishing higher.

History does not guarantee future results; adverse excursions (MAE) can be large even in winning windows.

Add it up: nine midterm election years, eight winners, a 72% cumulative return across those windows and a positive all-years average outcome. For traders who care about the calendar, this is one of the more consistent bullish stretches Devon has logged in the election cycle.

Price and near-term drivers

Devon Energy closed at 47.42 on Mar 18, up 1.65% on the day, with the stock trading about 0.2% below its 52-week high of 47.50 and well above its 50-day moving average of 41.55 on 18.4 million shares of volume.[1] The move caps a roughly 7.67% gain over the past month as investors digest the company’s planned all-stock merger with Coterra Energy, a $58 billion combination that would create a shale heavyweight in the Permian Basin.[1][4]

The merger, announced on Feb 2, is set to knit together two large U.S. shale producers into a single player with scale across key basins, including the Permian, Marcellus and Anadarko.[1][3][4][6][9] For Devon holders, the deal promises a broader asset base and potential cost synergies, but it also introduces integration risk and fresh exposure to gas-heavy acreage at a time when commodity prices remain volatile.

Strategically, the tie-up fits a broader consolidation wave in U.S. shale as producers seek scale, inventory depth and bargaining power with service providers.[4][9] Devon’s existing Permian footprint already offered high-rate-of-return drilling opportunities, and folding in Coterra’s assets could deepen that runway if management can execute on capital discipline and integration.

On the sell-side, Devon carries a Buy consensus rating, though the current TipRanks consensus price target of $43 sits below the market price and reflects an earlier, lower trading regime before the latest run toward 52-week highs.[2] That gap between target and tape underlines how quickly sentiment has shifted since late 2025 as investors have repriced the stock around the merger story and firmer energy equities.

The chart below situates the latest move in its recent multi-month context.

Macro and election-cycle backdrop

The upcoming window lands in the midterm election year, a phase that often brings policy uncertainty around regulation, taxes and energy policy. For a shale producer like Devon, that can translate into shifting expectations for drilling permits, pipeline approvals and potential changes in emissions rules, even if the underlying commodity tape remains the primary driver.

Industry-wide, consolidation has been a defining theme as producers respond to investor pressure for capital discipline and steady returns rather than pure volume growth.[4][9] Devon’s merger with Coterra positions the combined company as a dominant Permian player, with the scale to manage through policy swings and commodity cycles while still returning cash to shareholders if management sticks to its stated framework.[1][3]

In that context, the fact that Devon’s strongest seasonal window in the midterm year sits just ahead of the pre-election year is notable. Historically, risk assets have often found firmer footing as markets look past midterm noise toward the policy clarity and pro-growth bias that can accompany the year before the presidential election. For Devon, a stock already trading near its highs, the seasonal pattern suggests that this transition period has often been a tailwind rather than a headwind.

What to watch as the window opens

For traders tracking this pattern, the first checkpoint is simple: how Devon behaves as the window opens around Mar 22. A firm tone that holds the stock above its 50-day moving average and keeps it in the upper half of its recent range would be consistent with prior midterm-year springs. A quick break lower with a drawdown that starts to resemble the deeper adverse moves seen in 1994, 1998 or 2022 would signal that this iteration may be tracking one of the tougher historical years instead.

Second, watch how the merger narrative evolves. Any updates on regulatory review, synergy targets or capital-return plans from the combined Devon–Coterra entity could either reinforce or undercut the bullish seasonal backdrop.[1][4] Positive clarity on integration and cash returns during the window would rhyme with the strong historical pattern, while delays or negative surprises could be the catalyst that drives a rare losing year.

Third, price levels matter. On the upside, traders will be watching whether DVN can sustain a break above the 52-week high at 47.50 and build a base there rather than delivering a quick reversal. On the downside, how the stock behaves on pullbacks toward the 50-day moving average around 41.55 will help show whether any intraperiod drawdowns are routine noise or something more structural.

Finally, keep an eye on the broader policy and macro calendar as the midterm year unfolds. Headline risk around energy regulation, drilling permits or tax policy could inject volatility into a window that has historically been friendly to Devon longs. If the stock can absorb those shocks and still finish the 42-day stretch higher, it would mark yet another entry in a pattern that has already delivered eight wins out of nine.

Sources

- [1] The Wall Street Journal, "Devon Energy to Buy Coterra for $21.5 Billion to Create Shale Giant," Feb 2, 2026.

- [2] The Wall Street Journal, "Devon Energy to Buy Coterra for $21.5 Billion to Create Shale Giant," Feb 2, 2026.

- [3] Reuters, "US shale producers Devon and Coterra to merge in a $58 billion deal," Feb 2, 2026.

- [4] The Wall Street Journal, "Devon Energy to Buy Coterra for $21.5 Billion to Create Shale Giant," Feb 2, 2026.

- [5] Bloomberg, "Devon Agrees to Buy US Shale Rival Coterra for $21.4 Billion," Feb 2, 2026.